What’s the Meaning of an ABA Number and How to Find It

What is an ABA number? ABA numbers are numbers or American Bankers’ Association numbers, and they are essential for financial institutions when it comes to different transactions.

ABA figures are needed for all types of electronic bank-to-bank transfers. The range of activities covered by an ABA routing number includes paper check processing; electronic check processing through the Automated Clearing House (ACH) system; as well as wire transfer using the Fedwire system.

Let’s learn more about those!

What Comprises an ABA Number?

You already know what an ABA number is, the ABA meaning is clear, but what is it made of? It is composed of three sets of digits placed from left to right.

In simpler terms, this is made up of nine-digits that identify individual financial institutions. The bank account number identifies exactly which account the particular transaction goes with.

There is also a “fractional routing number” at the topmost section of every check, which can be used as an alternative should there be unforeseen problems with other routes.

Differentiating Between Routing Numbers and ABA Numbers

Is ABA the same as routing number? Actually, it is not. In most cases, however, people use the terms interchangeably with each other, though ABA numbers refer to a type of route code for banks.

However, it should also be noted that for some transactions such as wire transfers and certain kinds of automated clearing house (ACH) receipts, routing numbers may differ. To make sure you get things right when handling your finances, it would be helpful if you contacted your banking institution so that you know what specific routing code you need. So, the answer to the “Is ABA the same as routing number?” is negative.

Getting an ABA Number

Obtaining an American Bankers Association (ABA) involves following certain steps established by regulatory frameworks that govern financial institutions.

In case your depository institution carries a federal or state charter to hold an account at a Federal Reserve Bank, the process involves submitting an application form and paying requisite charges for it. This is how LexisNexis Risk Solutions issues ABA codes after merging with Accuity in February 2021.

Where to Find Your Bank’s ABA Number

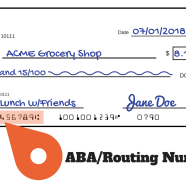

How to find my ABA routing number? If you want to know where your bank’s ABA number is located, just look at your checkbook. Printed in machine-readable magnetic ink (MICR), this nine-digit combination of numbers is the real address for money operations. Right next to that are two other very important numbers: the bank account and check numbers.

On each individual banking cheque, the lower left corner contains a bank transit ABA number written using magnetic ink character recognition technology which can be read by machines on automated processing systems. Also, there is a fractional variation of this number above the check line that gives even more detail including a unique set of numbers such as the branch code as well.

The relevance of these ABA routing numbers extends beyond paper checks themselves into deposit slips used for both savings accounts and checking accounts as well. However, one must note that certain banks may have multiple routing codes intended for different purposes thereby emphasizing why attention to detail matters when undertaking financial dealings.

Navigating Changes in ABA Numbers

The world of finance, characterized by mergers and acquisitions, necessitates the need to be on the lookout for any possible changes to your financial institution’s ABA number.

The American Bankers Association (ABA) Routing Number Lookup web page is an invaluable resource that can help mitigate uncertainties associated with these transitions. Your bank’s website or online banking application also contains important information, including the latest routing numbers for your financial transactions.

Utilization Across Various Transactions

There are many financial operations where various types of transactions take place; all of them depend on different reasons that make their usage significant beyond simply being some figures. Some involve:

- Check payments clearing: The functioning flow chart and quickness of clearing checks underpinning through the banking system within a minimum time span are done by means of arrangements relating to clearing checks using routing/bank transit ABA number.

- Electronic ACH transfers: This system processes digital transfers between banks located throughout America through which people can earn direct payment cash or pay bills immediately. This includes a wide variety of small business deposits versus electronic bill payments today to organizations such as large commercial banks.

- Wire transfers: In relation to wire transfers, fast cash movement from one account holder’s bank account to another person’s account has been made possible through ABA routing numbers, leading to the fastest, most convenient way of EFTs.

Integration with Federal Reserve Banks

The different ways in which ABA numbers are used by Federal Reserve banks include:

- Check services: The provision of digital and paper checks by the Federal Reserve Check Services is underpinned by ABA numbers. In this case, these services work from dedicated check processing centers that guarantee quick clearance and processing of checks both electronically as well as through traditional means involving use of papers.

- Fedwire funds service: In terms of wire transfers, the Fedwire funds service provided by the Federal Reserve Banks is a model for efficiency. This real-time gross settlement system operates using ABA numbers, enabling parties to move funds immediately on a final basis without recall, thereby enhancing the seamless movement of money within the financial network.

Why ABA Numbers are So Important

ABA numbers are more than figures; they are the backbone of financial transactions. Here’s why:

Financial Institutions Identification

By identifying banks, ABA numbers enable seamless processing of payments and direct deposit initiation. This is achieved by including check routing numbers within the ABA numbers, which ensures accuracy in money transfers.

Assignment of Unique Identifiers

State and federally-chartered U.S. banks with reserve accounts at Federal Reserve Banks, as well as other financial institutions, have their own individual ABA number, too. These serve as key elements for handling checks, electronic payments, along with ACH direct deposits thereby providing fundamental services upon which modern finance is based upon.

In this way, ABA numbers act as silent partners in the financial world making sure that money keeps flowing efficiently between different institutions and across various platforms while preserving its sanctity.

Finding Your ABA Number without a Check

When it comes to finding your ABA number, usually checks provide easy access, but sometimes you might find yourself without one. Do not worry, though; there are other means to obtain this critical routing number. Here’s how:

- Bank statement: When you look at your bank statement, you can see some hints that will be helpful to you. In the right column towards the top side note down your account number. Now focus on the third and fourth digits of your account number – these two can determine which routing number is assigned to your bank.

- Bank’s website: Reach your bank’s website so that you can find it there. If you are not sure, ask a customer service representative.

- Local bank inquiry: Your local bank can help you with that. Most banks will provide this information online, but you may need to sign in to your account for the details. Watch out for things about direct deposits or see anything different on your bank’s website regarding Automated Clearing House (ACH). Alternatively, call their customer care desk and inquire.

- ABA Online Lookup Tool: Use the latest technology available through the ABA online lookup tool; it will be worth it as it gives you various routing numbers directly from there. Be careful, though, because there is a limit – only two ABA numbers per day and no more than ten within a 30-day period. Remember, too, that some states and transactions may have separate numbers.

When ABA Codes are Acting

Once again, although you may not use your ABA routing number every day, it is necessary for a few important transactions, including:

- Direct deposits via ACH: As a new entrant into employment, you will be required to provide your account number and the ABA routing number so that direct deposits can be made through ACH. This will make your salary disbursement process shorter.

- Wire transfers: For seamless execution of wire transfers, whether sending or receiving, especially in international transactions, you must have your ABA routing number.

- IRS direct Deposits: This makes the Internal Revenue Service (IRS) directly deposit returns, hence fast-tracking repayment by requiring your routing numbers.

- Bill payments: To ensure that there is no struggle to meet financial obligations through mobile payment apps or online bill payments, use your routing numbers.

- Retirement account deposits or bank transfers: Facilitating smooth transactions involves establishing an Automated Clearing House (ACH) transfer for retirement savings or moving funds from one bank to another by using the bank’s route numbers.

However cryptic the ABA code might seem, this is what links us to most of our daily financial activities today. Now, you know everything: from how to find my ABA routing number to the most common usage cases.